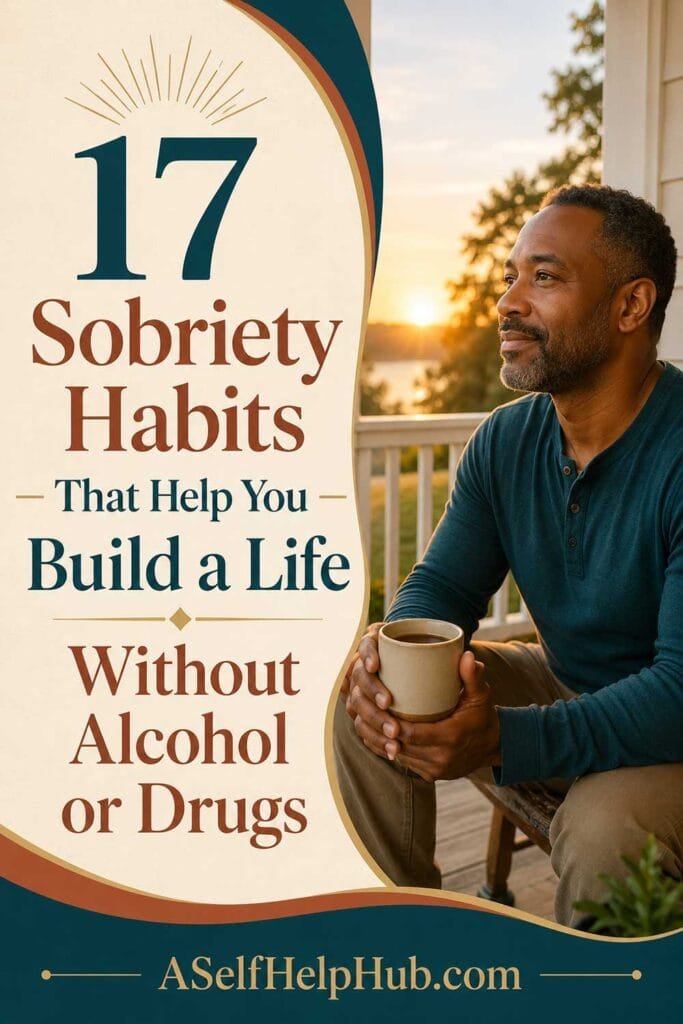

17 Personal Finance Tips for People Managing a Tight Budget

Managing a tight budget does not mean you are failing at money. It means you are doing something incredibly hard and doing it every single day without giving up, making difficult decisions with limited options and figuring out how to stretch what you have further than it feels like it should go.

These 17 personal finance tips cover stretching limited income, cutting costs without cutting joy, and building small financial habits that create real breathing room even when the numbers feel impossibly tight. A tight budget is not a dead end. It is a starting point for someone who is about to find out exactly how resourceful they truly are.

Free Download: The Money Reset Workbook

The person who learns to manage a little money well is always the one best prepared to manage a lot of it, and the Money Reset Workbook gives you the spending tracker, budget, and savings planner to start managing what you have with real clarity. Download it free today.

Get the Free Money Reset Workbook1. Track Every Dollar for One Full Month Before Changing Anything

“A tight budget is not a dead end, it is a starting point for someone who is about to figure out exactly how resourceful they truly are.”

Most tight budget problems are partly a visibility problem. When you do not know exactly where every dollar goes, the money disappears faster than the math suggests it should. One full month of tracking every single dollar spent, even the smallest purchases, produces an honest picture that almost always reveals at least two or three spending areas where small changes would produce real breathing room. The tracking does not change anything immediately. The picture it produces changes everything.

2. Build Your Budget From Essential Needs First

A budget built from wants to needs tends to leave the essentials under-funded. A budget built from essential needs first, housing, utilities, food, transportation, and minimum debt payments, ensures the critical obligations are covered before any discretionary allocation is made. Whatever remains after the essentials is the actual discretionary budget, even if that amount is very small. Knowing the real number removes the false sense that there is more flexibility than there is.

3. Find the One Spending Category Where a Small Change Produces the Most Relief

“The person who learns to manage a little money well is always the one best prepared to manage a lot of it.”

Across-the-board budget cuts are hard to sustain because they require constant deprivation in every area simultaneously. Identifying the single category where a modest, specific change would produce the most financial relief, and focusing only there first, produces results with minimal willpower while avoiding the budget burnout that trying to cut everything at once reliably creates. One change. Sustained. Then the next one.

Visit Premier Print Works

Keep the reminder that a tight budget is a starting point, not a dead end visible where your daily financial decisions happen. Premier Print Works offers prints, mugs, and art for the person doing hard financial work every single day. Visit the shop today.

Visit Premier Print Works4. Use Cash Envelopes or a Debit-Only System for Variable Spending

When spending is done with a physical cash or debit system, the finite nature of what is available becomes impossible to ignore in the way that credit or digital payment can obscure. Assigning a specific cash amount to each variable spending category for the week and stopping when the envelope is empty, however uncomfortable that stopping may be, provides a natural hard limit that the brain responds to differently than an abstract account balance.

5. Meal Plan Around Sales and What Is Already in Your Pantry

Meal planning built around what is on sale and what is already in the pantry rather than around desired meals and then grocery shopping accordingly, reverses the relationship between what you want to cook and what you can afford to cook in a way that consistently reduces the grocery bill without reducing the quality of what gets made. Planning the week’s meals after checking the sale flyer and taking a pantry inventory is a simple reorder of steps that produces a meaningfully different spending outcome.

6. Access Free and Low-Cost Community Resources

Public libraries offer books, audiobooks, digital media, computer access, and increasingly free programming and classes. Community organizations offer food banks, free health clinics, utility assistance programs, and other services that exist specifically for people managing limited income. Using the resources that are available for exactly this situation is not a source of shame. It is resourceful use of the community infrastructure built to support people in tight financial stretches.

How Amara and Joel Found Breathing Room Where They Had Not Expected to Find It

Amara and Joel had been managing a genuinely tight budget for several months and had reached the point where the tightness felt structural rather than temporary, like there was simply not enough money rather than like there was money going somewhere unhelpful. Both felt the situation more as a fixed reality than as something with room for adjustment.

The tracking exercise revealed something they had not expected. There was one specific spending category, not the obvious ones they had already addressed, where small accumulated purchases were producing a weekly total that surprised both of them when they saw it as a number rather than as individual small decisions that had felt minor in the moment.

Cutting that one category by half produced enough monthly relief to fund a small emergency savings amount for the first time. The emergency fund felt significant not because of the amount, which was modest, but because of what it represented: the beginning of a financial cushion where there had been none, built from money that had been present all along and simply invisible without the tracking that made it visible.

7. Lower Your Utility Bills With Free Behavioral Changes

“A tight budget is not a dead end, it is a starting point for someone who is about to figure out exactly how resourceful they truly are.”

Utility costs can be reduced meaningfully through behavioral changes that cost nothing: turning off lights when leaving rooms, adjusting the thermostat by a few degrees, washing clothes in cold water, air-drying dishes rather than using the heated dry cycle, and unplugging devices when not in use. None of these individually produces dramatic savings. Accumulated across a full month and sustained over a year, they produce a utility bill that is noticeably lower than the one produced by default habits.

8. Negotiate With Service Providers Before Assuming the Rate Is Fixed

Internet providers, cell phone carriers, insurance companies, and many other recurring service providers have retention offers available to customers who call and express an intention to switch or cancel. A ten-minute phone call asking whether there is a better rate available is among the highest-value uses of time available to anyone managing a tight budget, and the answer is more often yes than the assumption that rates are fixed suggests.

9. Find Free Entertainment and Social Activities

A tight budget does not require a joyless life. Public parks, hiking trails, free museum days, library programs, community events, beach visits, home dinner parties, and many other genuinely enjoyable activities cost nothing or very little. Deliberately building a repertoire of free activities that you genuinely enjoy protects social connection and personal wellbeing without the financial cost of entertainment options that assume a discretionary budget that is not currently available.

Free Download: The 9 Daily Habits Checklist

Managing a tight budget is supported by the consistent daily habits that keep you intentional and forward-moving even when the resources feel limited. The free 9 Daily Habits Checklist gives you nine proven daily practices to build alongside your financial goals. Download it free today.

Get the Free Habits Checklist10. Save Even a Dollar a Day When That Is What Is Available

“The person who learns to manage a little money well is always the one best prepared to manage a lot of it.”

The habit of saving, even in amounts that feel too small to matter, builds the muscle that sustains saving at larger amounts when they become possible. A dollar a day is thirty dollars a month and three hundred and sixty-five dollars a year, which is not nothing, and is considerably more than zero, which is what saving nothing produces. The amount matters less than the habit. The habit is what scales when the income eventually does.

11. Look for Ways to Add Even Small Additional Income

When the budget is tight on both sides, the income side deserves as much attention as the expense side. Selling unused items, taking on a few hours of freelance work in any area of existing skill, driving for a rideshare service, offering a specific service in the local community, or any other approach to generating additional cash in available time adds to what is available without requiring the expense side to do impossible work alone.

12. Apply for Every Assistance Program You Qualify For

Government and nonprofit assistance programs exist for people managing limited income, including food assistance, utility assistance, housing support, childcare subsidies, healthcare programs, and many others. Applying for programs you qualify for is not an imposition on a system meant for someone else. It is using resources specifically designed for the situation you are in, and using them reduces the financial pressure that otherwise prevents all other progress.

How Joel’s One-Dollar-a-Day Habit Changed What He Believed Was Possible

Joel had convinced himself that saving was not available to him at his current income level, that the amount he could set aside was too small to be worth the effort or the sacrifice, and that saving was something he would do when the income was higher. The reasoning felt sound and had been preventing him from saving anything for longer than he was comfortable admitting.

He tried the one dollar a day experiment without expecting much. The first week felt insignificant. The first month produced thirty dollars in a separate account that had not been there before. The amount was not impressive. The fact that it existed at all was. He had believed saving was not possible. The thirty dollars was specific, concrete evidence that it was.

He increased to two dollars a day the following month. Then to five. The amounts remained modest for a long time. The habit was consistent for a long time, and the consistent habit was what eventually made the larger amounts feel natural rather than heroic. The person who manages a little money well, he had discovered, is indeed the one best prepared to manage more of it, because the habit does not care about the size. The habit cares about the repetition.

13. Use Generic and Store Brand Products Everywhere They Are Equivalent

Store brand and generic products in the categories where the quality difference from the name brand is minimal or nonexistent, pantry staples, cleaning supplies, paper products, over-the-counter medications, and many others, produce consistent savings without any reduction in the actual outcome they deliver. Switching systematically in the categories where quality is genuinely equivalent recovers spending that was going to brand premium rather than to what the product actually does.

14. Cook at Home as the Default Rather Than the Backup

“A tight budget is not a dead end, it is a starting point for someone who is about to figure out exactly how resourceful they truly are.”

The per-meal cost gap between cooking at home and purchasing prepared food, whether restaurant, delivery, or even many convenience items, is significant enough that a shift from eating out as the default to cooking at home as the default produces one of the largest budget impacts available in a typical household. Even imperfect home cooking, the simple meals that take fifteen minutes and use affordable ingredients, consistently costs a fraction of the cheapest restaurant equivalent.

15. Review Your Bills Annually and Look for Cheaper Alternatives

Annual reviews of insurance policies, phone plans, internet plans, and other recurring services, comparing current rates against available alternatives, consistently produce opportunities to reduce costs without reducing the service itself. Markets change, promotional rates expire and new ones become available, and competitors regularly offer lower prices for comparable coverage. The annual review is the mechanism that catches the savings that inertia quietly prevents.

16. Build a Baby Emergency Fund of One Thousand Dollars First

Before working on any other financial goal, building even a small emergency fund, one thousand dollars being the commonly cited starting target, changes the financial risk profile of the household in a meaningful way. Without it, any unexpected expense becomes a debt event. With it, most ordinary emergencies can be absorbed without derailing the budget entirely. The thousand dollars does not take long to accumulate with focused effort and provides disproportionate financial stability for its size.

17. Give Yourself Credit for Doing Something Genuinely Hard

“The person who learns to manage a little money well is always the one best prepared to manage a lot of it.”

Managing a tight budget is genuinely difficult, requiring daily decisions under constraint that people with more financial margin simply do not face. The shame that often accompanies financial tightness is misdirected. The difficulty is not a character flaw. It is a structural reality, and the person navigating it every day with intention, tracking, and consistent small decisions is doing something that deserves to be acknowledged as the hard and worthy work that it is. Give yourself that credit. You are building something real, and you are doing it in harder conditions than you deserve.

A Tight Budget Is Not a Dead End — It Is Proof of How Resourceful You Truly Are

Track every dollar for one month. Build your budget from essential needs first. Find the one category where a small change produces the most relief. Use cash or debit for variable spending. Meal plan around sales and your pantry. Access free community resources. Lower utility bills with free behavioral changes. Negotiate with service providers. Find free entertainment. Save even one dollar a day. Look for ways to add small additional income. Apply for every assistance program you qualify for. Use generic products where they are equivalent. Cook at home as the default. Review bills annually. Build a baby emergency fund first. Give yourself credit for doing something genuinely hard. Seventeen tips. A tight budget is a starting point for someone about to discover exactly how resourceful they are, and the person who learns to manage a little money well is always the one best prepared to manage a lot of it.

Free Download: The Money Reset Workbook

Start using these personal finance tips to make every dollar work harder and take back control of your finances no matter where you are starting from. The free Money Reset Workbook gives you the spending tracker, budget, and savings planner to build from. Download it free today.

Get the Free Money Reset WorkbookOur Top Picks for a Better Life

We have gathered our favorite tools, resources, and recommendations for making every dollar count and building financial breathing room even from a tight starting point. Everything we trust enough to share, all in one place.

See Our Top Picks

Financial Encouragement at Premier Print Works

Keep the reminder that the person who learns to manage a little money well is always the one best prepared to manage a lot of it, visible where your daily financial decisions happen. Visit Premier Print Works for prints, mugs, and art for the person doing hard financial work every day.

Visit Premier Print WorksDisclaimer

The content on A Self Help Hub is for informational and inspirational purposes only. The personal finance tips and personal stories in this article offer general support for everyday money management. They are not professional financial advice, tax advice, benefits counseling, or any form of licensed financial planning.

Individual financial situations vary widely. If you are in significant financial hardship, please consider reaching out to a nonprofit credit counseling agency, a financial social worker, or other qualified professional who can provide guidance specific to your situation. Many free and low-cost services are available. Please do your own research regarding assistance programs, as eligibility rules and available programs vary by location and change over time.

The stories and composite characters in this article, including Amara and Joel, are illustrative. They are based on common experiences and created to make the content relatable. They are not real people. Any resemblance to a specific person is coincidental.

Some links on this site, including links to Premier Print Works, may be affiliate links. A Self Help Hub may earn a small commission at no extra cost to you. We only recommend things we genuinely believe in.

All content on A Self Help Hub is copyrighted. You may not copy or republish it without written permission. By reading this article you agree to this disclaimer.