7 Money Saving Tips That Help You Get Back on Track Financially

The financial off-track moment arrives in different forms for different people — the unexpected expense that wiped out the savings that had taken months to build, the season of reduced income that required the credit card to cover the basics, the gradual drift of the spending that went unnoticed until the month-end picture was significantly different from what had been assumed. However the getting-off-track happened, the feeling that accompanies it is reliably similar: the specific combination of the shame of the not-having-done-better and the overwhelm of the not-knowing-where-to-start that together produce the specific paralysis of the person who knows something needs to change and cannot yet see what to do next.

Getting off track financially does not make you a failure — it makes you human, and the only thing that matters now is what you decide to do next. It does not matter how slowly you go as long as you do not stop — and that is as true for your finances as it is for anything else in life. Every financial comeback starts with one honest look at where you are and one brave decision to do something different. You are not too far gone and it is never too late to get back on track. Start with one tip today and let the momentum carry you forward. The following seven tips are the starting point.

Free Download: The Money Reset Workbook

The financial reset begins with the honest picture — and the free Money Reset Workbook gives you the step-by-step framework to build it. Track the income, identify where the money has been going, and build the simple financial plan that puts you back in the driver’s seat. The Money Reset Workbook is the practical starting point for the financial comeback these seven tips are pointing toward. Download it free today.

Get the Free Money Reset Workbook1. Stop the Bleeding Before Trying to Build

“Every financial comeback starts with one honest look at where you are and one brave decision to do something different. The first brave decision is the stopping of the outflow that has been exceeding the inflow. Stop first. Build after.”

The financial comeback that begins with the ambitious savings goal before the spending that exceeded the income has been addressed is the comeback built on a foundation that is still actively crumbling. The building on the crumbling foundation produces the specific frustration of the person who is saving twenty dollars while spending thirty dollars more than they earn — the net movement is still in the wrong direction regardless of the saving. The first step of the financial reset is not the building — it is the stopping of the active financial bleeding that is producing the getting-off-track in the first place.

Look at the current spending honestly and identify the categories where the outflow has been exceeding what the income can support. Not the entire spending picture at once — the specific categories where the overspending is most significant and most immediately addressable. The subscription that has not been used in months and that continues to charge the credit card. The dining category that has grown significantly past the level the income supports. The recurring purchase that felt manageable in isolation and that together with the other recurring purchases is the specific source of the monthly shortfall. Stop the most significant bleeding first. The building follows the stopping. Stop first.

“Identify the most significant active bleeding and stop it first. The building follows the stopping. The building on the still-bleeding foundation produces the frustration of the net movement in the wrong direction.”

2. Do the No-Spend Challenge for Seven Days

“It does not matter how slowly you go as long as you do not stop — and the seven-day no-spend challenge is the stop that creates the pause long enough to see where the spending has actually been going and to experience the specific relief of the week without the drift.”

The seven-day no-spend challenge — the commitment to spend money during the week only on the genuine necessities that cannot be avoided — is the financial reset tool that most directly interrupts the spending patterns that have been running on autopilot without the deliberate attention that would have caught the drift. The challenge is not the permanent austerity — it is the specific pause that creates the visibility. The week without the discretionary spending reveals which discretionary spending was genuinely wanted and which was the habitual convenience that the deliberate week without it demonstrates can be done without.

The seven-day no-spend challenge serves two simultaneous functions: it generates the immediate financial breathing room of the week’s discretionary spending not going out, and it produces the specific self-knowledge of the spending patterns that were too automatic to be seen clearly before the pause that makes them visible. At the end of the seven days, most people have learned something specific about where the money has been going that the previous months of the unexamined spending had not revealed. The challenge is the pause. The pause is the visibility. The visibility is the beginning of the deliberate choice about what the spending restarts with.

“Do the seven-day no-spend challenge. The pause creates the visibility. The visibility is the honest picture. The honest picture is the beginning of the deliberate reset.”

3. Cancel or Pause Every Non-Essential Subscription

“The subscriptions that have been accumulating without the regular review are the specific form of the spending drift that is most invisible in the daily life and most visible in the monthly statement. Review them all. Cancel what is not genuinely used. The freed money is the immediate result of the fifteen-minute audit.”

The subscription audit is the financial reset action with the highest ratio of immediate impact to time invested — because the subscriptions that have been accumulating, each individually justified at the moment of the sign-up and each individually forgotten in the daily life that moved on from it, together represent a monthly outgoing that most people underestimate by a significant amount. The streaming service signed up for the specific show and never cancelled. The fitness app downloaded during the motivated January and still charging in October. The software subscription for the project that finished eight months ago. Each small. Together the monthly total that the audit makes visible.

Audit every subscription in the next fifteen minutes. Go to the bank statement or the credit card statement of the last two months and mark every recurring charge. For each one: is this being used regularly? Is the use worth the monthly cost? If the honest answer to either question is no, cancel today. Not pause — cancel. The paused subscription is the subscription that will be forgotten about and restarted automatically. The cancelled subscription is the freed money. The freed money from the subscription audit is often more than expected. Redirect every freed dollar to the financial reset fund or the emergency fund. The subscription audit is the fifteen minutes that changes the monthly picture.

Visit Premier Print Works

Keep the reminder that the financial comeback is being built — one honest decision at a time, one freed dollar at a time — visible in the spaces where the daily money decisions happen. Premier Print Works offers prints, mugs, and art designed for the person doing the patient, courageous work of taking back control of their finances — honest, motivating pieces for the home where the rebuild begins every day.

Visit Premier Print WorksHow Clem Stopped the Bleeding and Started the Comeback That Changed Her Financial Story

Clem had been off track financially for fourteen months when she finally stopped avoiding the honest picture and looked at it. The avoiding had felt like the protection from the specific shame of the not-having-managed-better — the belief that the looking would confirm the worst version of the story she had been telling herself about her relationship with money. The looking confirmed a different story. She had not been reckless. She had been inattentive — specifically to the subscriptions, the small recurring charges, and the dining spending that had each grown individually in the months after the income disruption that had started the off-track season without any single decision to let them.

The subscription audit took her twenty-two minutes and identified eleven recurring charges she had not been actively thinking about. She cancelled eight of them immediately. The freed monthly total from the cancellations alone was more than she had been putting in savings in any given month. She had not needed to earn more. She had needed to stop the outflow she was not seeing. The seven-day no-spend challenge that followed the audit produced the specific relief of the week where the spending choices were deliberate rather than automatic — and the specific clarity, at the end of the seven days, about which spending she genuinely missed and which she had been doing on autopilot without the genuine wanting.

She did not achieve the dramatic financial transformation in ninety days. She achieved the specific, real, measurable progress of the person who stopped the bleeding, did the honest audit, and made the first three deliberate decisions rather than the continued automatic ones. By the end of the first three months she had rebuilt the emergency fund to five hundred dollars — the first five hundred dollars she had held in savings in over a year. The amount was not large. The feeling it produced was disproportionate to the amount, because the five hundred dollars was not the number — it was the evidence that the financial story was being rewritten from the deliberate position rather than the drifting one. The comeback had started the day she looked at the numbers instead of avoiding them.

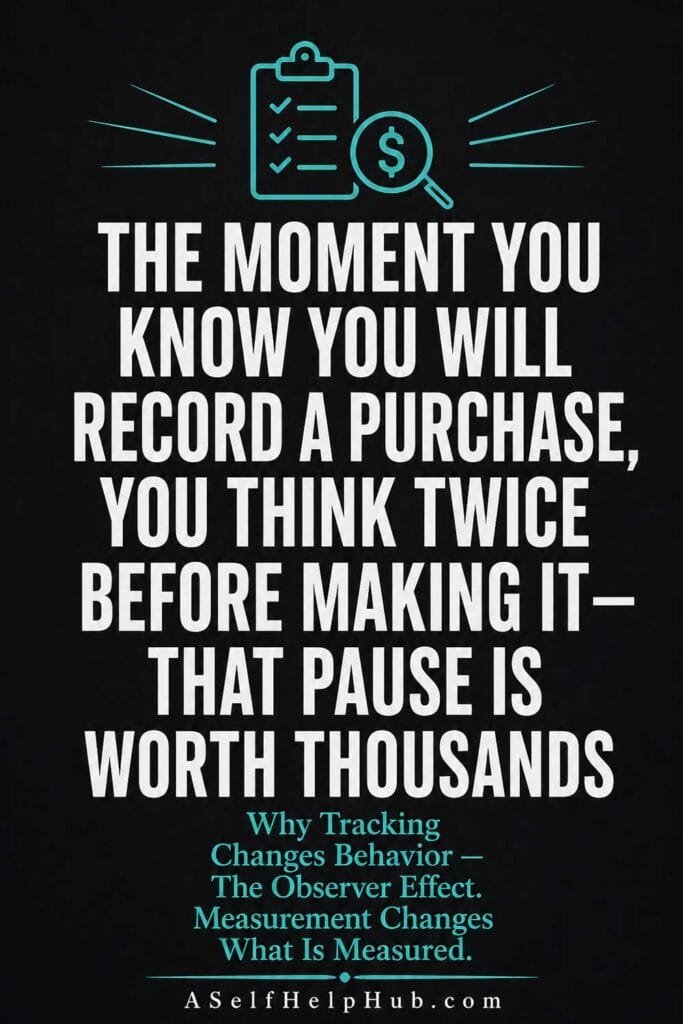

4. Use the Cash Envelope Method for the Three Categories Where You Overspend Most

“The cash in the envelope is the spending limit that the card swipe does not enforce. The envelope that empties is the signal the low-balance notification rarely sends in time. For the categories where the overspending is most consistent, the physical limit changes what the psychological limit could not.”

The cash envelope method — the practice of withdrawing the budgeted amount in cash for the specific spending categories where the overspending is most consistent and spending from the physical cash rather than the card — is the financial reset tool that most directly addresses the specific psychology of the overspending in the categories that have been most difficult to manage. The card swipe conceals the running total in a way the diminishing cash does not. The person who has fifteen dollars left in the dining envelope at the end of the second week of the month has the clear, immediate, unavoidable picture of the remaining category budget. The person who has fifteen dollars left on the credit card available for dining in the same situation does not have the same clarity.

Identify the three categories where the overspending has been most consistent — the categories that the monthly review most reliably reveals as over budget. For each of those three categories, withdraw the budgeted amount in cash at the beginning of the month. Spend from the cash. When the cash is gone, the spending in that category stops for the month. The first month of the cash envelope method is the month that reveals the gap between the budgeted amount and the actual spending pattern in a way that the card statement review cannot — because the running out of the physical cash is more viscerally informative than the discovering of the overage at the month’s end. Adjust the budget based on what the first cash month reveals.

“Use cash for the three categories where overspending is most consistent. The physical limit enforces what the psychological limit could not. The empty envelope is the clearest budget feedback available.”

5. Find One Recurring Bill to Negotiate, Reduce, or Eliminate This Week

“You are not too far gone and it is never too late to get back on track — and the phone call that reduces the monthly bill is the specific, available, immediately impactful action that most people do not take because the asking feels awkward and the savings feel uncertain. Make the call. The savings are more certain than they appear.”

The recurring bills that have been accepted at their current amount without the challenge — the internet, the phone, the insurance, the utility — are the specific category where the spending reduction is most accessible with the least friction. The service providers that most people pay without question are the service providers that most frequently have the promotional rate, the loyalty discount, or the competitor price-match available to the customer who calls and asks. The asking is the action most people are not taking because the outcome feels uncertain. The outcome is less uncertain than it appears: most service providers have the retention tools to offer the customer who calls to discuss the bill.

Choose one recurring bill this week and make the call. Tell the provider that the bill is higher than what fits the current budget and ask what options are available to reduce it. Ask specifically whether there are promotional rates, loyalty discounts, or lower-tier plans that would reduce the monthly cost. Be willing to mention the competitor pricing if there is a competitor option. The call takes fifteen minutes. The savings from the successful call appear every month for as long as the reduced rate applies. The worst outcome from the call is the same bill. The best outcome is the monthly savings that required only the asking. Make the call this week.

“Make the call about one recurring bill this week. Ask for the reduction. The worst outcome is the same bill. The best outcome is the monthly savings that required only the asking.”

Free Download: The 9 Daily Habits Checklist

The financial comeback is sustained by the daily habits that keep the intentional spending and the consistent saving going through every ordinary week — the small, daily money choices that add up to the financial stability being rebuilt. The free 9 Daily Habits Checklist gives you the daily structure that supports the financial habits alongside every other important daily practice. Download it free.

Get the Free Habits Checklist6. Automate a Small Savings Transfer the Day the Paycheck Arrives

“The savings that is transferred automatically before the spending begins is the savings that happens. The savings planned from what remains after the spending is the savings that usually does not. Automate the transfer. Make the savings happen before the spending has the chance to prevent it.”

The automatic savings transfer — the specific, scheduled movement of a fixed amount from the checking account to the savings account on the day the paycheck arrives — is the single most reliable mechanism for rebuilding the savings after the getting-off-track, because it removes the monthly decision that the getting-off-track has demonstrated is vulnerable to the competing demands of the month’s spending. The savings that happens automatically happens regardless of whether the month has been expensive or whether the motivation for saving is high. The savings that depends on the motivation and the month having been manageable rarely happens consistently.

Set up the automatic transfer today. The amount does not need to be large to be effective — twenty-five dollars per paycheck, transferred automatically to the savings account the day the paycheck arrives, is twenty-five dollars building the foundation that the financial comeback requires. Start with an amount small enough to be genuinely sustainable through the difficult months as well as the easy ones. Increase the amount as the financial situation stabilizes and the additional margin becomes available. The habit of the automatic saving, maintained consistently and increased gradually, is the mechanism that rebuilds the financial foundation. The automatic transfer makes the habit happen. Make it happen automatically.

“Automate the savings transfer for the day the paycheck arrives. Start small enough to be sustainable. The automatic transfer makes the savings happen before the spending prevents it.”

Rebuilding Financially Alongside Recovery? This Is for You.

For some people, the work of getting back on track financially is happening alongside the daily practice of sobriety — where the financial rebuilding and the recovery are the same courageous work done from the same starting point at the same time. If that is where you are, the free Sober Survival Guide offers honest support for the person doing both kinds of rebuilding at once. Download it free.

Get the Free Sober Survival Guide7. Measure Progress in Weeks, Not Months

“The financial comeback measured monthly feels slow. The financial comeback measured weekly feels like it is moving. The week is the unit the momentum is built from. Measure the week. Let the weeks build the months.”

The financial comeback that is measured monthly is the comeback that is measured at the cadence that makes progress feel slowest — because the month is a long enough period that the individual week’s progress is diluted in the average, and the month that contains one expensive unexpected week alongside three careful weeks may show less progress than the careful weeks actually produced. The weekly measurement keeps the progress visible at the level where it is actually happening — the specific week that stayed within the cash envelope, the week that made the savings transfer, the week that did not add to the credit card balance.

Measure the financial comeback weekly. Not the full budget review every week — the specific check-in on the week’s most important financial behaviors. Was the cash envelope method followed this week? Was the savings transfer made? Were any subscriptions cancelled or bills negotiated? Did the week end with the credit card balance the same or lower than it began? These weekly measurements are the specific, immediate, controllable evidence of the comeback in progress — the evidence that the monthly measurement would have diluted into the average. Track the weeks. Let the weeks of the genuine progress accumulate into the months that tell the comeback story. The momentum is built in the weeks. Measure what builds the momentum.

“Measure the comeback in weeks. The week is the unit where the momentum is built and visible. The months are built from the weeks. Track the weeks. Let the weeks build the story.”

How Ridley Rebuilt the Financial Foundation He Thought Was Too Far Gone to Recover

Ridley had been telling himself for eight months that the financial situation was too far gone to address without the dramatic intervention — the windfall, the income increase, the some-specific-thing-changing that would create the conditions in which the recovery was possible. The telling of this story had been the specific mechanism that allowed the eight months to pass without the one honest look at where he was and the one brave decision to do something different. The dramatic intervention was the requirement the story was using to excuse the not-beginning.

The beginning, when it finally came, was not dramatic. It was a Saturday afternoon with a notebook and the last two months of the bank statements — the specific, uncomfortable, overdue look at where the money had actually been going. The looking revealed not the catastrophe the avoidance had been protecting him from confronting but the very specific, very addressable pattern of the money going to predictable places through the automatic behaviors that had never been examined because the examination was the thing that had been avoided. The subscriptions. The dining. The small recurring charges that together were the gap between the income and the spending.

He did three things in the first week: cancelled six subscriptions, committed to the seven-day no-spend challenge, and set up the twenty-five dollar automatic savings transfer for the day each paycheck arrived. The three actions required approximately ninety minutes of the total time. The combined financial effect in the first month was more meaningful than anything he had done in the previous eight months of the waiting for the dramatic intervention. The intervention was not dramatic. It was available. It had been available the entire time. The only thing that had been unavailable was the Saturday afternoon with the notebook and the willingness to look at the numbers. The looking was the beginning. The beginning was all that had ever been required to start.

Picture the Financial Foundation Being Rebuilt One Week at a Time

Not the dramatic transformation — the genuine, measurable, building-from-where-you-are comeback. The week where the bleeding was stopped. The week where the subscription audit freed the monthly dollars that had been going unnoticed. The week where the automatic savings transfer was set up and the first twenty-five dollars went somewhere deliberate instead of somewhere automatic. The week where the cash envelope ran out and the staying within it felt, for the first time in months, like the evidence of the control rather than the absence of it.

You are not too far gone. It is never too late to get back on track. Start with one tip today. Let the momentum of the starting carry you to the next one. The comeback starts with the one honest look and the one brave decision. You have already taken the honest look by reading this far. The brave decision is the next thing. Make it today.

Free Download: The Money Reset Workbook

Put these seven tips into practice with the step-by-step framework of the free Money Reset Workbook. Build the honest financial picture, identify where the money has been going, and create the simple plan that puts the comeback in motion. Download it free and take the first real step back toward financial stability today.

Get the Free Money Reset WorkbookOur Top Picks for a Better Life

We have gathered our favorite tools, resources, and recommendations for getting back on track financially, building better money habits, and creating the financial foundation that puts the future back in control — everything we trust enough to share, all in one place.

See Our Top PicksFinancial Comeback Prints at Premier Print Works

Keep the reminder that the comeback is in progress — one honest decision, one freed dollar, one week of the deliberate spending at a time — visible in the spaces where the daily money decisions happen. Visit Premier Print Works for prints, mugs, and art designed for the person rebuilding their financial foundation with the patient courage the comeback requires.

Visit Premier Print WorksDisclaimer

The content published on A Self Help Hub is provided for informational, educational, and inspirational purposes only. The money saving tips, financial perspectives, and personal stories shared in this article are intended to offer general guidance for people who are working to improve their personal financial situations. They do not constitute professional financial advice, investment advice, debt counseling, credit counseling, or legal advice of any kind. A Self Help Hub is not a licensed financial advisor, credit counselor, or professional financial planning organization.

Individual financial situations vary significantly and depend on many factors including income, existing debt, cost of living, financial obligations, and personal circumstances that are outside our knowledge or control. The money saving tips and general strategies described in this article are general starting points and may not be appropriate for every financial situation. If you are experiencing significant financial distress, significant debt, or situations involving collections, foreclosure, or bankruptcy, we strongly recommend consulting with a qualified financial professional, credit counselor, or legal advisor who can provide guidance specific to your individual circumstances.

The personal stories and composite characters featured in this article, including Clem and Ridley, are illustrative in nature. They are drawn from a combination of common financial experiences and narrative examples created to make the content relatable and accessible. They are not presented as factual accounts of specific individuals, and any financial outcomes described are examples only and not guarantees or typical results.

Some links on this site, including links to Premier Print Works and other recommended resources, may be affiliate or partner links through which A Self Help Hub earns a commission at no additional cost to you. We only recommend products and resources we genuinely believe in and would share regardless of any compensation received.

The Sober Survival Guide and any recovery-related content linked from this site is provided as general supportive information only. It is not a substitute for professional addiction treatment, clinical intervention, medical detox, or licensed counseling services. If you or someone you love is struggling with addiction or substance use, please seek the care of a qualified healthcare or addiction treatment professional. Recovery is possible and professional support significantly improves outcomes.

If you are experiencing a mental health crisis, thoughts of self-harm, or are in immediate danger, please do not rely on this content for support. Contact emergency services, a crisis helpline, or a qualified mental health professional immediately. You deserve real, immediate help — and it is available to you.

All content on A Self Help Hub is the copyrighted property of A Self Help Hub. You may not copy, reproduce, or republish our content without prior written permission. By reading this article you acknowledge that you have read and agree to this disclaimer.