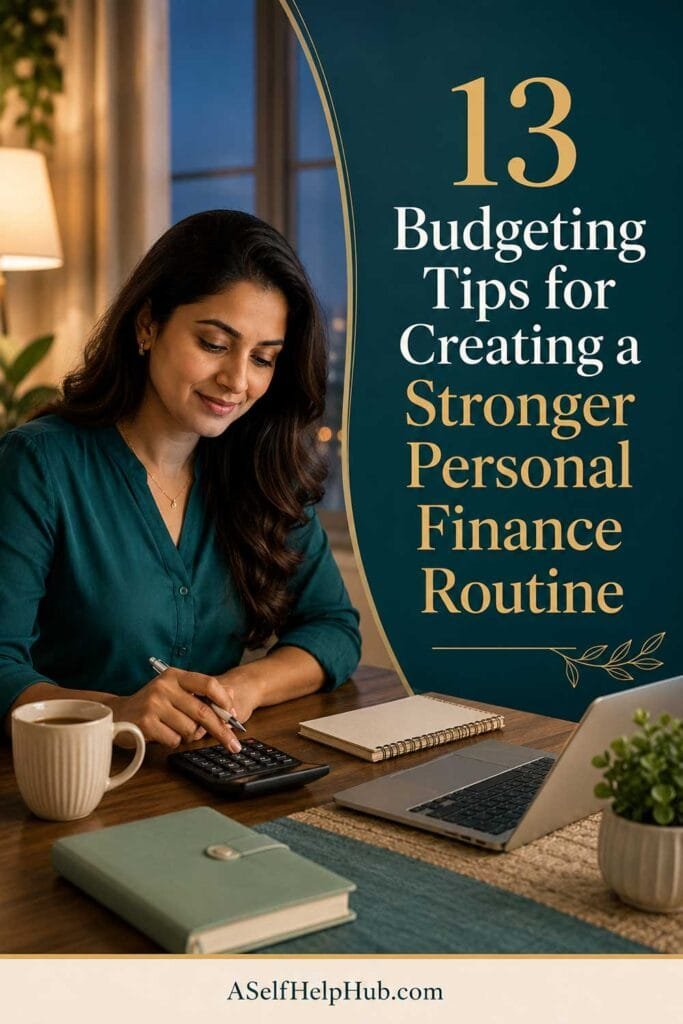

7 Emergency Fund Tips That Help You Build a Financial Safety Net

An emergency fund is not just a financial tool. It is the buffer between a bad day and a financial crisis. Without one, a single unexpected expense can unravel months of careful budgeting and push you toward debt you did not plan for and may spend a long time climbing out of.

These seven tips walk through how to start small, stay consistent, and build a safety net that gives you real confidence when unexpected expenses show up. You do not need to build it all at once. You only need to start.

Free Download: The Money Reset Workbook

An emergency fund is not pessimism, it is preparation, and the free Money Reset Workbook gives you the tools to plan, track, and build that safety net with real clarity. It includes a savings goals planner, a spending tracker, and a simple budget to build from. Download it free today.

Get the Free Money Reset Workbook1. Start With a Small Target, Not the Full Three to Six Months

“An emergency fund is not pessimism, it is preparation.”

The standard advice to save three to six months of expenses is correct as a long-term goal and paralyzing as a starting point. Start with a target of one thousand dollars instead. That smaller number is achievable quickly enough to build real momentum, and it provides genuine protection against the most common minor emergencies that derail most budgets.

2. Open a Separate Account Specifically for the Emergency Fund

An emergency fund kept in the same account as everyday spending is not truly protected. It is too easy to dip into for non-emergencies when the balance is sitting there visibly. Open a separate savings account, label it clearly, and treat that separation as a real boundary. Out of sight reduces the temptation to use it for anything other than a genuine emergency.

3. Automate the Transfer So It Happens Before You Spend

“The greatest financial gift you can give yourself is a cushion that buys you time.”

Set up an automatic transfer to your emergency fund account on the same day your paycheck arrives, even if the amount is small. Money that moves before you see it is money that gets saved reliably. A fifteen-dollar automatic transfer, repeated consistently, builds a real cushion over time without requiring willpower at every pay period.

Visit Premier Print Works

Keep the reminder that the greatest financial gift you can give yourself is a cushion that buys you time visible where you do your financial planning. Premier Print Works offers prints, mugs, and art for the person building their financial safety net. Visit the shop today.

Visit Premier Print Works4. Define What Counts as a Real Emergency Before One Arrives

Without a clear definition, the emergency fund becomes the fund for anything uncomfortable or inconvenient. A car repair, a medical bill, or a sudden job loss qualifies. A sale you do not want to miss, an unexpected social event, or a purchase you just really want does not. Writing down your definition before an expense arrives removes the in-the-moment negotiation that erodes the fund.

How Amara and Joel Finally Built the Cushion They Had Always Talked About

Amara and Joel had talked about starting an emergency fund for years without ever actually starting one. The full three-to-six-month target felt so distant that beginning never felt urgent enough to prioritize, so it stayed on the list of things they would get to eventually.

They finally set a target of one thousand dollars only, opened a separate account labeled Emergency Only, and set up a twenty-five dollar automatic transfer every payday. Neither change felt significant in the moment.

Eleven months later, their car needed an unexpected repair. They paid for it without touching a credit card and without the panic that had followed every previous unexpected expense. The fund had not been large. It had simply been there, separate and untouched, exactly when they needed it. The years of talking about it had never produced that feeling. The small consistent action had.

5. Rebuild the Fund Immediately After Using It

“An emergency fund is not pessimism, it is preparation.”

The fund’s value comes from being available when the next emergency arrives, not just the last one. As soon as you use any portion of it, restart the automatic transfer and treat rebuilding as the immediate next financial priority. An emergency fund at zero is a budget with no protection, and the next unexpected expense rarely waits long.

6. Direct Windfalls and Unexpected Income Toward the Fund

Tax refunds, bonuses, cash gifts, and small one-time earnings are among the fastest ways to close the gap between where your emergency fund currently stands and where it needs to be. Decide in advance that any windfall income goes directly to the fund until it is fully built. The decision made in advance is far more reliable than the one made in the moment of receiving extra money.

Free Download: The 9 Daily Habits Checklist

Building a financial safety net is supported by the consistent daily habits that keep your financial plan on track. The free 9 Daily Habits Checklist gives you nine proven practices to build that consistency into your routine. Download it free today.

Get the Free Habits Checklist7. Track the Balance Monthly and Celebrate the Milestones

An emergency fund grows in the background, quietly and without fanfare, which makes it easy to underestimate the real progress being made. Check the balance monthly and acknowledge each milestone, the first two hundred fifty dollars, the first five hundred, the full thousand. Recognizing the progress makes the habit sustainable across the full time it takes to build genuine protection.

Your Emergency Fund Is the Confidence That Your Future Self Will Be Grateful For

Start with a small target. Open a separate account. Automate the transfer. Define what counts as a real emergency. Rebuild immediately after using it. Direct windfalls toward it. Track the balance and celebrate milestones. Seven tips. An emergency fund is not pessimism, it is preparation, and the greatest financial gift you can give yourself is a cushion that buys you time.

Free Download: The Money Reset Workbook

Start building the financial safety net your future self will be grateful for. The free Money Reset Workbook gives you the tools to plan, track, and grow your emergency fund with real clarity. Download it free today.

Get the Free Money Reset WorkbookOur Top Picks for a Better Life

We have gathered our favorite tools, resources, and recommendations for building an emergency fund and a financial safety net that gives you real peace of mind. Everything we trust enough to share, all in one place.

See Our Top Picks

Financial Safety Net Reminders at Premier Print Works

Keep the reminder that an emergency fund is not pessimism, it is preparation visible where your financial planning happens. Visit Premier Print Works for prints, mugs, and art for the person building real financial confidence.

Visit Premier Print WorksDisclaimer

The content on A Self Help Hub is for informational and inspirational purposes only. The tips and personal stories in this article offer general support for everyday financial habits and personal development. They are not professional financial advice, tax advice, or any form of licensed financial planning.

If you are dealing with significant debt, financial hardship, or major financial decisions, please speak with a qualified financial advisor or credit counselor. General self-help content is not a substitute for professional financial guidance.

The stories and composite characters in this article, including Amara and Joel, are illustrative. They are based on common experiences and created to make the content relatable. They are not real people. Any resemblance to a specific person is coincidental.

Some links on this site, including links to Premier Print Works, may be affiliate links. A Self Help Hub may earn a small commission at no extra cost to you. We only recommend things we genuinely believe in.

All content on A Self Help Hub is copyrighted. You may not copy or republish it without written permission. By reading this article you agree to this disclaimer.