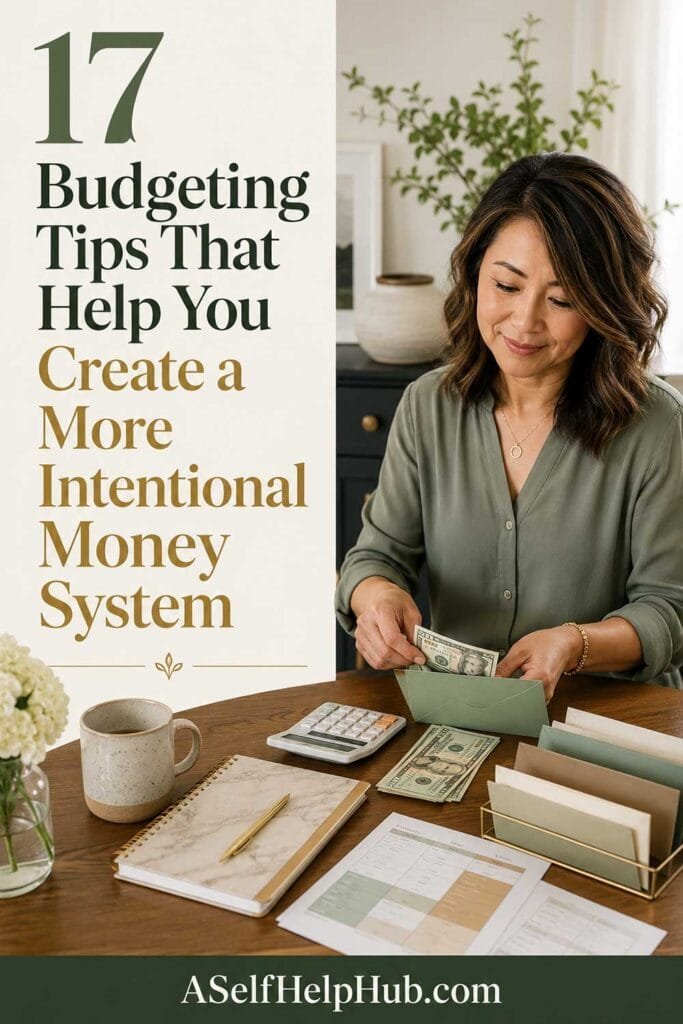

13 Budgeting Habits That Help You Spend With More Intention

Most people think of a budget as a restriction. A list of things they cannot have. A ceiling that makes life smaller. That version of budgeting produces resentment and abandonment in roughly equal measure, because deprivation is not a sustainable financial strategy and it was never the point of a budget in the first place.

Intentional spending is different. It is the practice of deciding in advance where your money goes so that the decisions you make with it reflect what you actually care about rather than just the defaults, impulses, and inertia that fill the gaps when you have not decided. These 13 budgeting habits build that practice. They are not about spending less. They are about spending better, in ways that feel more like you and less like something that just happened to your bank account this month.

Free Download: The Money Reset Workbook

Intentional spending starts with a clear picture of where your money is going and where you want it to go instead. The free Money Reset Workbook gives you a practical spending tracker, budget template, and values-based planning framework to build your intentional spending practice from. Download it free today.

Get the Free Money Reset Workbook1. Write your values before you write your budget.

“Intentional spending is the practice of deciding in advance where your money goes so that the decisions you make with it reflect what you actually care about, not just the defaults that fill the gaps.”

The most powerful budgeting habit is the one that happens before the budget itself: getting honest about what you actually value. Not what you think you should value or what sounds responsible to say you value. What you genuinely care about when you are being honest with yourself. Freedom. Security. Experiences. Connection. Health. Creative expression. Family. Whatever is on your real list is the list your budget should be built to serve. A budget that is not connected to anything you genuinely value is a set of arbitrary restrictions. A budget that is directly connected to what you care most about is a tool for building the life you want. Start with the values. Build the budget from there.

2. Budget before the month begins, not halfway through it.

A budget made on the first of the month is a plan. A budget made on the fifteenth is a post-mortem. The habit of building next month’s budget in the last few days of the current month, before the money has arrived and before the spending has begun, is the habit that converts budgeting from a review of what went wrong into a decision about what goes right. The decisions made in advance, from a calm and intentional place, are almost always better than the decisions made in the moment with the money already in the account and the opportunity to spend it already present.

3. Track every purchase for one full month before adjusting anything.

“A budget made on the first of the month is a plan. A budget made on the fifteenth is a post-mortem. Build the plan before the month, not during it.”

The most common budgeting mistake is setting spending limits before you have accurate data about your actual spending. Build the data first. Spend one month tracking every purchase honestly, without trying to change anything, and see what the real numbers are. The gap between what you think you spend and what you actually spend is almost always larger than expected in at least two or three categories, and the information that gap provides is worth more than any budget you could build from guesswork. Track first. Budget from the truth.

Visit Premier Print Works

The daily reminders of what you are spending toward matter as much as the budget itself. Premier Print Works offers prints, mugs, and art for people building more intentional financial habits and a daily life that reflects what they actually value. Visit the shop today.

Visit Premier Print Works4. Assign every dollar a category before the month starts.

Zero-based budgeting, where income minus all assigned categories equals zero, is one of the most effective budgeting frameworks for intentional spending because it eliminates the gray area where unintentional spending lives. Every dollar that enters your account has a job assigned to it before it arrives: rent, groceries, savings, entertainment, debt payment. The dollar that has not been assigned a job is the dollar that funds the impulse purchases, the forgotten subscriptions, and the end-of-month mystery of where it all went. Assign the job first. The unassigned dollar is the source of most unintentional spending.

5. Build a guilt-free spending category into every budget.

A budget without a category for spending on things you genuinely enjoy, without tracking, without justifying, without feeling bad, is a budget that will be abandoned. The guilt-free category is not a weakness in the intentional spending plan. It is what makes the plan sustainable. The amount in this category should be realistic rather than token, enough to feel like genuine permission rather than a consolation prize. When the money in the guilt-free category is spent, it is spent freely and without regret. When it is gone, it is gone until next month. The rest of the budget stays intact because the pressure valve exists.

6. Check your budget before making any significant unplanned purchase.

“The guilt-free category is not a weakness in the intentional spending plan. It is what makes the plan sustainable. Permission to enjoy some of your money is what keeps the rest of the plan honest.”

The habit of checking the budget before making any significant unplanned purchase, not after, replaces the reactive spending decision with an intentional one. The question is simple: is this in the budget? If yes, spend it freely. If not, decide consciously whether the budget can accommodate it this month or whether it needs to wait. The check takes thirty seconds. It converts what would have been an unconscious decision into a conscious one. Conscious decisions made consistently produce a fundamentally different financial life than unconscious ones. The budget check is the moment where the intention happens.

7. Do a ten-minute weekly money check-in.

A weekly ten-minute review of where the budget stands, what has been spent, what remains in each category, and what the coming week looks like financially, keeps the intentional spending practice alive in a way that a monthly review cannot. The monthly review shows you what happened. The weekly check-in gives you the opportunity to adjust course before the month is over and the decisions have already been made. The ten minutes is enough to catch a category that is running ahead of plan and redirect spending before it becomes a problem. Consistent weekly check-ins make the monthly review feel like a confirmation rather than a surprise.

8. Separate needs, wants, and aligned wants before you spend.

“A weekly ten-minute money check-in gives you the opportunity to adjust course before the month is over. The monthly review shows you what happened. The weekly check-in lets you change it.”

Not all wants are equal and treating them as though they are leads to spending that feels neither satisfying nor intentional. A more useful framework separates wants into two categories: wants that are aligned with your values, things you genuinely care about that bring real satisfaction, and wants that are not, things that happen out of habit, boredom, or social pressure without producing meaningful satisfaction. The intentional spending habit is to redirect unaligned wants toward aligned ones without eliminating enjoyment entirely. Spend freely on the things you actually care about. Scrutinize the things you are spending on without caring about them. The distinction changes where the money goes in ways that feel like more life rather than less of it.

9. Make savings the first line in the budget, not the last.

The budget that saves whatever is left after spending is the budget that almost never saves anything, because spending expands to fill available income with impressive consistency. The intentional budgeting habit of placing savings at the top of the budget, the first category that is funded before any discretionary spending begins, converts saving from an aspiration into a non-negotiable. Automate the transfer on payday and the savings happen before the spending has the opportunity to use the money instead. The savings are not what is left. The savings are what comes first.

10. Review your subscriptions every quarter.

“Savings that are placed at the top of the budget and automated on payday are not what is left after spending. They are what comes first. This single reversal changes the outcome more than any other single budgeting habit.”

Subscriptions are the spending category most likely to become unintentional over time. A service subscribed to with genuine purpose gradually becomes a service that is paid for out of inertia rather than use. A quarterly subscription audit, fifteen minutes of going through every recurring charge and asking whether it is being actively and valuably used, consistently recovers money that was leaving without delivering anything in return. The savings found in a quarterly subscription audit are not dramatic in any individual instance. Over a year of quarterly reviews they are reliably significant. Cancel what you are not using. Redirect that money to something you actually care about.

11. Eat before you grocery shop and shop with a list.

The grocery store is the budgeting category where intention is most easily defeated by hunger, convenience, and excellent retail design. Two simple habits eliminate most of the overspending: never shop hungry and always shop with a specific, written list. The hungry shopper buys more, buys higher-margin items, and abandons the plan in favor of whatever looks good at eye level. The shopper with a list buys what is on the list and resists the strategic placement of everything else. These two habits together can reduce grocery spending by a meaningful percentage with no reduction in the quality or quantity of food, simply by removing the conditions that make unintentional grocery spending so consistent and so invisible.

12. Talk about the budget with your partner if you share finances.

“Never shop hungry and always shop with a specific written list. Two habits, no sacrifice, consistently meaningful savings in the budget category most vulnerable to unintentional spending.”

Shared finances that are not discussed regularly become a source of conflict that is really a source of different and unspoken values producing incompatible spending decisions. A brief monthly money conversation with a partner, fifteen to twenty minutes reviewing the budget together, discussing priorities for the coming month, and acknowledging any tensions between individual spending preferences and shared financial goals, is the budgeting habit that prevents the slow accumulation of financial resentment that unspoken money differences produce. The conversation does not have to be perfect. It has to happen. Regular, honest, low-stakes money conversations are one of the most underestimated contributors to both financial success and relationship health.

13. Measure success by direction, not perfection.

The budget that was followed in eight of thirteen categories is a more successful budget than the one that was planned perfectly and never used. The month where two unintentional purchases happened but everything else was intentional is a more intentional month than the month where nothing was tracked at all. Measuring your progress against a standard of perfect execution guarantees both failure and the abandonment of the practice when the inevitable imperfect month arrives. Measure against the direction instead. Is the spending more intentional this month than last? Is the gap between what you value and where the money goes closing rather than widening? That direction is the success. Keep moving in it.

How Daniel and Amara Each Found the Budgeting Habit That Changed How Their Money Felt

Daniel had been budgeting in the conventional sense, tracking spending after it happened and feeling vaguely unsatisfied by the results, for two years without the practice producing any meaningful change in his financial life. The shift came when a financial podcast he listened to made a distinction that reoriented everything: tracking is not budgeting. Tracking tells you what happened. Budgeting is the decision made before it happens. Daniel started building his budget in the last week of each month for the following month, before the money arrived. The first month he did it he noticed something he had never noticed before: the act of deciding where the money would go before it arrived changed what he did with it once it did. He had made the decisions from a calm place rather than a reactive one. The money went where he had decided. The satisfaction with where it went was completely different from anything the after-the-fact tracking had ever produced.

Amara’s habit was writing her values before writing her budget. She had been budgeting for years without being able to explain why it felt meaningless even when she followed it. A therapist who worked on financial wellbeing alongside emotional wellbeing suggested that the missing piece might be the connection between the budget and anything she actually cared about. Amara spent an hour one evening writing an honest list of what she valued most. The list surprised her. The budget she built the following month, aligned directly with that list for the first time, felt different from every budget she had built before it. Not easier. Different. She was building toward something she recognized. The money was going where her actual life was, not where the default categories suggested it should go. That recognition was the difference between budgeting as discipline and budgeting as intention. She had been missing the latter for years without knowing it was the thing that had been missing.

The Financial Life You Want Is Built From the Choices You Make Intentionally. These Habits Are How You Make Them.

Intentional spending is not a financial technique. It is a daily practice of treating your money as the finite, powerful resource it is and making conscious decisions about where it goes rather than discovering where it went after the fact.

The thirteen habits in this article build that practice from different angles. You do not need all thirteen. You need the two or three that address the specific places where your spending becomes unintentional. Build those. Let them produce the clarity and satisfaction that intentional spending produces. Then add more when you are ready.

The financial life that reflects your actual values is one intentional decision at a time closer than it was before you started. Keep making the decisions.

Free Download: The Money Reset Workbook

Let these budgeting habits be the reminder that every dollar is a choice you get to make. The free Money Reset Workbook gives you the practical tools to track your spending, build a values-based budget, and start spending with the intention your financial life deserves. Download it free today.

Get the Free Money Reset WorkbookOur Top Picks for a Better Life

We have gathered our favorite tools, resources, and recommendations for building intentional spending habits, smarter budgeting practices, and a financial life that feels like yours. Everything we trust enough to share, all in one place.

See Our Top Picks

Intentional Spending Reminders at Premier Print Works

Keep the reminders of what your money is building visible in your daily life. Visit Premier Print Works for prints, mugs, and art for people who are spending with more intention and building a financial life that reflects what they genuinely value.

Visit Premier Print WorksDisclaimer

The content on A Self Help Hub is for informational and educational purposes only. The budgeting habits and personal stories in this article offer general guidance for everyday financial wellness and are not professional financial advice, investment advice, tax advice, or any form of regulated financial planning or counsel.

Every person’s financial situation is unique. Before making significant financial decisions, please consult with a qualified financial advisor, accountant, or other licensed professional who can assess your specific circumstances. General self-help content is not a substitute for professional financial guidance.

The stories and composite characters in this article, including Daniel and Amara, are illustrative. They are based on common experiences and created to make the content relatable. They are not real people. Any resemblance to a specific person is coincidental.

Some links on this site, including links to Premier Print Works, may be affiliate links. A Self Help Hub may earn a small commission at no extra cost to you. We only recommend things we genuinely believe in.

If you are in a mental health crisis or thinking about self-harm, please do not rely on this content for support. Contact emergency services or a crisis helpline right away. You deserve real help and it is available to you now.

All content on A Self Help Hub is copyrighted. You may not copy or republish it without written permission. By reading this article you agree to this disclaimer.